Most Common Business Policies

Running a towing company in New York means dealing with risks most business owners never consider. A routine roadside assist can turn into a $50,000 liability claim if a customer's vehicle gets damaged on your hook. A workplace injury at your lot could cost you six figures in medical bills and lost wages. New York's insurance requirements for towing operations are among the strictest in the country, and the penalties for non-compliance include losing your operating authority entirely.

Whether you're running a single flatbed out of Brooklyn or managing a fleet of heavy-duty wreckers across upstate counties, understanding your insurance needs isn't optional. It's the foundation of staying in business. The right coverage protects your equipment, your employees, your customers' vehicles, and your personal assets when something goes wrong. The wrong coverage, or gaps you didn't know existed, can wipe out everything you've built.

This guide breaks down what New York towing companies actually need, what drives your premium costs, and how to get proper protection without overpaying. You'll find specific requirements, real coverage scenarios, and practical strategies that work in New York's unique regulatory environment.

Understanding New York State Insurance Requirements

New York regulates towing companies more heavily than most states. You'll answer to multiple agencies, each with their own requirements and paperwork. Getting this wrong doesn't just mean fines: it can shut down your operation entirely.

Minimum Liability and No-Fault Coverage

New York mandates specific minimum coverage amounts for commercial vehicles. Tow trucks require at least $1.25 million in combined single limit liability coverage for bodily injury and property damage. This exceeds standard commercial auto minimums because of the inherent risks in towing operations.

You'll also need Personal Injury Protection coverage under New York's no-fault insurance system. This covers medical expenses for anyone injured in your tow truck, regardless of who caused the accident. The minimum is $50,000, though many carriers recommend higher limits given typical medical costs in the state.

Uninsured and underinsured motorist coverage is also mandatory. Given that roughly 6% of New York drivers operate without insurance, this protection matters more than you might expect.

USDOT and NYSDOT Compliance Standards

If your tow trucks cross state lines or haul vehicles over certain weight thresholds, you'll need USDOT registration. This brings federal Motor Carrier Act requirements into play, including maintaining proof of insurance through Form MCS-90 filings.

NYSDOT has its own registration requirements for intrastate operations. Your insurance certificates must list the correct MC and DOT numbers, and carriers must file proof of coverage directly with the state. Lapses in coverage get reported automatically, triggering immediate investigation and potential suspension of your operating authority.

Essential Coverage Types for Towing Operations

Beyond state minimums, towing companies face exposures that require specialized policies. Standard commercial auto insurance leaves significant gaps that can devastate your business after a single incident.

On-Hook Coverage for Client Vehicles

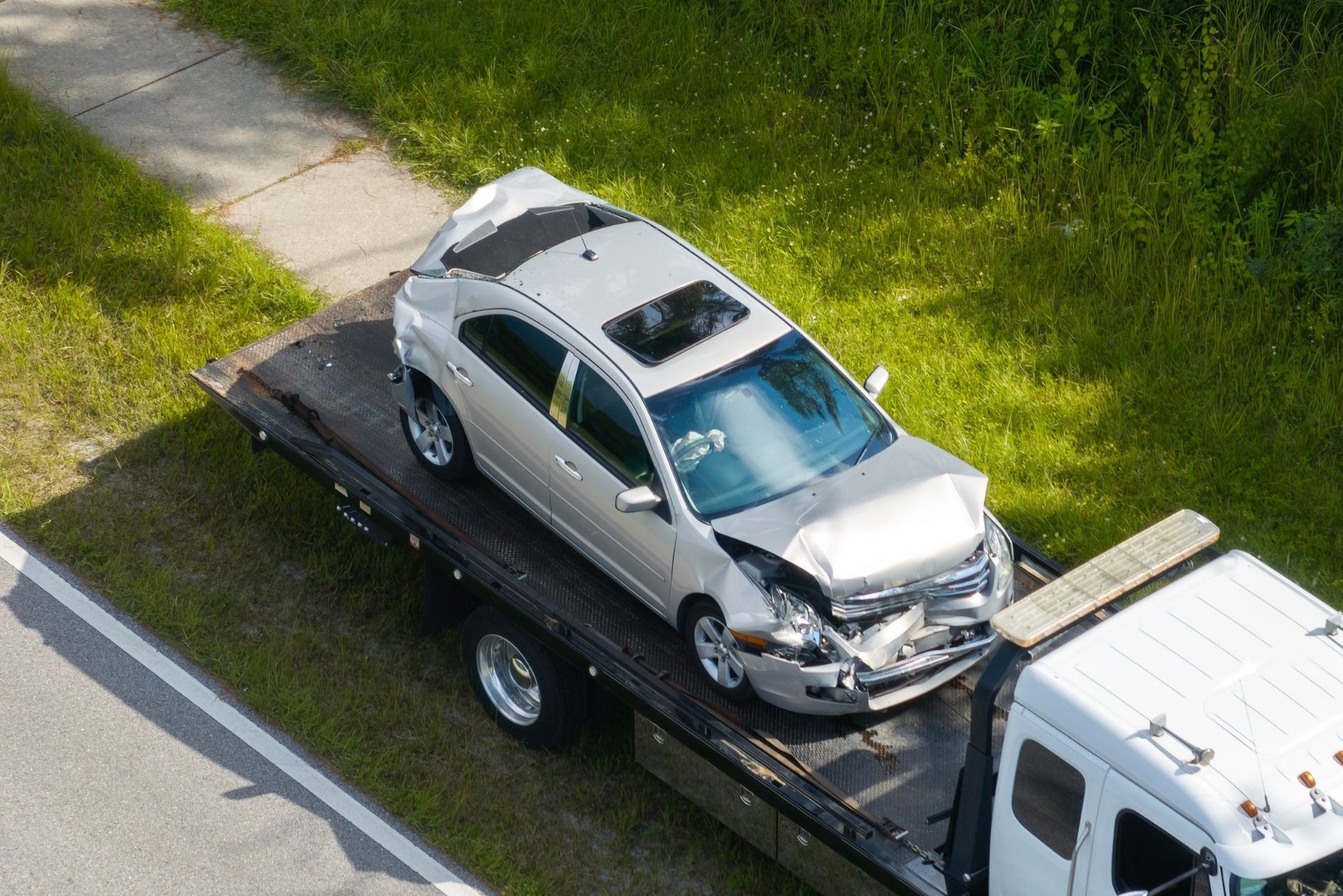

On-hook coverage protects vehicles while they're being towed. This is separate from your commercial auto liability and covers damage to the customer's car, truck, or motorcycle from the moment you hook it until delivery.

Standard policies range from $50,000 to $150,000 per occurrence. If you tow luxury vehicles, classic cars, or commercial equipment, you'll need higher limits. A single damaged Mercedes or restored muscle car can exceed basic coverage quickly. Some insurers offer tiered on-hook coverage based on vehicle value categories.

Garagekeepers Legal Liability

Once a vehicle reaches your lot, on-hook coverage ends. Garagekeepers liability takes over, protecting stored vehicles against fire, theft, vandalism, and collision while in your care.

| Coverage Type | What It Protects | Typical Limits |

|---|---|---|

| On-Hook | Vehicles during towing | $50,000-$150,000 |

| Garagekeepers | Vehicles in your lot | $100,000-$500,000 |

| Direct Primary | Covers regardless of fault | Higher premiums |

| Legal Liability | Only when you're negligent | Lower premiums |

Direct primary garagekeepers coverage pays claims even when you're not at fault, while legal liability versions only respond when negligence is proven. The premium difference is substantial, but direct primary eliminates coverage disputes.

General Liability and Property Protection

General liability covers third-party injuries and property damage from your business operations outside of vehicle accidents. A customer slipping on your lot, a damaged fence during a recovery, or a lawsuit from a disputed tow all fall under this policy.

Most New York towing companies need at least $1 million per occurrence with a $2 million aggregate.

Property coverage protects your building, equipment, tools, and office contents. Don't forget business income coverage: if a fire destroys your garage, you'll still have loan payments, payroll, and fixed costs while rebuilding.

Factors Influencing Insurance Costs in New York

Towing insurance premiums in New York run 20-40% higher than national averages. Understanding what drives your specific costs helps you make strategic decisions about coverage and operations.

Geographic Location and Service Areas

Operating in New York City versus rural Adirondack counties creates dramatically different risk profiles. NYC towing companies face higher theft rates, more frequent accidents, and greater exposure to liability claims. Premiums reflect this reality.

Your primary service area matters too. Highway contracts carry higher premiums than parking lot enforcement. Accident scene towing exposes you to secondary collisions and injured parties. Insurers price these risks individually, so your specific mix of services shapes your premium more than simple location.

Fleet Size and Equipment Value

Every truck you add increases your premium, but not linearly. Insurers often offer fleet discounts starting at three to five vehicles. The type of equipment matters significantly: a heavy-duty rotator valued at $400,000 costs far more to insure than a standard flatbed worth $60,000.

Age factors in as well. Newer trucks with advanced safety features often qualify for discounts. Trucks over ten years old may face surcharges or coverage restrictions. Maintaining detailed records of your equipment's condition and safety features helps during renewal negotiations.

Driver History and Safety Records

Your drivers' MVRs directly impact premiums. Each driver with accidents, violations, or DUIs on their record increases your costs. Some insurers won't cover drivers with certain violation histories at all.

Company-wide safety records matter too. Your loss history over the past three to five years is the single biggest factor in your premium calculation. One large claim can increase rates for years. Conversely, a clean claims history qualifies you for experience credits that compound over time.

New York requires workers' compensation coverage for virtually all employees, with no minimum employee threshold. Towing companies face classification codes that reflect the hazardous nature of the work, resulting in higher per-$100-of-payroll rates than many other industries.

Tow truck operators typically fall under classification code 7219, which carries rates between $8 and $15 per $100 of payroll depending on your experience modification factor. A company with $300,000 in annual payroll could pay $24,000 to $45,000 for workers' comp alone.

New York also mandates disability benefits insurance, covering non-work-related injuries and illnesses. This runs about $0.60 per $100 of weekly payroll. While less expensive than workers' comp, missing this coverage triggers fines and personal liability for the business owner.

Paid Family Leave is another mandatory coverage, funded through employee payroll deductions but administered through your disability carrier. Keeping these coverages coordinated prevents gaps and compliance issues.

High premiums don't have to be permanent. Strategic investments in safety and documentation can reduce costs significantly over two to three years.

Implementing Safety and Training Programs

Formal safety programs demonstrate commitment to loss prevention. Insurers reward documented training with premium credits ranging from 5-15%. Your program should include initial driver training, regular refresher courses, and specific protocols for high-risk operations like heavy-duty recovery.

Drug testing programs, both pre-employment and random, qualify for additional discounts. Background checks and MVR monitoring show insurers you're actively managing driver risk. Keep detailed records of all training: certificates, attendance logs, and test results all support your renewal negotiations.

Installing Dash Cams and GPS Tracking

Dash cameras protect you from fraudulent claims and provide evidence when you're not at fault. Many insurers offer 5-10% discounts for fleet-wide camera systems. The footage also helps train drivers by reviewing near-misses and identifying risky habits.

GPS tracking demonstrates operational control and helps recover stolen vehicles. Some carriers factor tracking systems into their underwriting, particularly for

high-value equipment. The investment typically pays for itself through insurance savings within 18-24 months.

Selecting the Right New York Insurance Provider

Not all insurance carriers understand towing operations. Working with the wrong provider means coverage gaps, claim disputes, and premiums that don't reflect your actual risk profile.

Look for carriers with specific towing industry experience. They'll understand on-hook exposures, motor club contracts, and the unique liability situations you face. Ask potential insurers how many towing companies they cover in New York and what their claims process looks like for typical scenarios.

Independent agents who specialize in commercial transportation often provide better options than direct carriers or general business agents. They can access multiple markets, compare coverage forms, and advocate during claims. The commission structure is the same whether you go direct or through an agent, so the expertise costs you nothing extra.

Review policy exclusions carefully. Some carriers exclude certain tow types, impose radius restrictions, or limit coverage for specific equipment. A policy that looks affordable might leave you exposed exactly when you need protection most.

Frequently Asked Questions

How much does towing company insurance cost in New York? Annual premiums typically range from $8,000 to $25,000 per truck, depending on coverage limits, location, and claims history. NYC operators generally pay toward the higher end.

Can I operate with just the state minimum coverage? Technically yes, but minimums leave dangerous gaps. One serious claim could exceed your coverage and expose personal assets.

What happens if my insurance lapses? NYSDOT receives automatic notification. Your operating authority gets suspended, and you'll face fines plus higher premiums when you reinstate.

Do I need separate coverage for each type of towing? Not separate policies, but your policy must specifically cover all services you provide. Light-duty, medium-duty, and heavy-duty operations have different rating factors.

How long do claims affect my premiums?

Most insurers look at three to five years of loss history. Large claims can impact rates for the full period.

Making the Right Choice for Your Business

Getting towing insurance right in New York requires balancing compliance requirements, adequate protection, and manageable costs. The state's strict regulations and high-risk operating environment make this more complex than in most markets.

Start by ensuring you meet all mandatory coverages: commercial auto liability, on-hook, workers' comp, disability, and paid family leave. Then evaluate your specific exposures for garagekeepers, general liability, and excess coverage. Work with specialists who understand towing operations and can identify gaps before they become expensive lessons.

Your insurance should grow with your business. Review coverage annually, update vehicle schedules promptly, and maintain the safety documentation that earns premium credits. The investment in proper protection lets you focus on running your operation instead of worrying about the next claim.

ABOUT THE AUTHOR:

JELANI FENTON

As Owner of EG Bowman, I’m dedicated to continuing a legacy of trust and excellence built over more than seven decades. My focus is on helping businesses and individuals secure reliable, forward-thinking insurance solutions that protect their assets and support long-term growth.

Contact Us

OUR SERVICES

New York Business Insurance Coverage

General Liability Insurance

Workers Comp Insurance

Commercial Property Insurance

Commercial Auto Insurance

Commercial Umbrella Insurance

Business Owner's Policy

OUR SERVICES

New York Personal Insurance Coverage

Auto Insurance

Get coverage for your car and protect yourself on the road. We provide options for accidents, damages, and more.

Home Insurance

Protect your home and belongings with coverage for damages, theft, and unexpected events.

Umbrella Insurance

Extend your coverage with umbrella insurance for extra protection when you need it most.

Condo Insurance

Get peace of mind with condo insurance that protects your space and personal belongings.

NEW YORK BUSINESSES WE WORK WITH

Industries We Serve In New York

Electrician Insurance

Get coverage that protects electricians from accidents, property damage, and liability risks. Keep your tools, equipment, and business safe with plans designed for your needs. Request a quote to stay covered and focused on your work.

Real Estate Developer Insurance

Protect your projects with insurance that covers construction risks, liability, and property damage. We offer plans to keep your developments secure and on track. Get a quote to ensure your business is protected.

Wholesaler and Distributor Insurance

Protect your inventory and business operations with insurance that covers property damage and liability risks. Keep your supply chain running without disruptions. Get a quote to safeguard your business today.

What is an independent insurance agency, and how does it differ from a traditional insurance company?

An independent insurance agency works with multiple insurance carriers instead of just one. This allows us to provide customized coverage options tailored to your needs, rather than offering a one-size-fits-all policy. Independent agencies focus on finding the best value and coverage for their clients by comparing policies across various providers. At EG Bowman, we pride ourselves on offering personalized service and expertise to ensure our clients get the coverage that fits their specific needs.

What types of insurance does EG Bowman offer?

EG Bowman offers a wide range of insurance solutions, including commercial insurance, personal lines, property insurance, liability insurance, and specialized policies tailored to niche industries. Our focus is on protecting businesses and individuals from unforeseen risks. Whether you're looking for coverage for your home, car, or business, our team works to provide the most comprehensive and competitive options available. We’re here to make sure you’re prepared for the unexpected.

How does EG Bowman help businesses with insurance?

We specialize in understanding the unique risks businesses face and crafting insurance solutions to address them. From general liability to workers' compensation and industry-specific policies, our team ensures your business is protected at every level. We also provide risk management consultations to identify potential vulnerabilities and recommend solutions. With decades of experience, EG Bowman acts as a trusted partner, helping businesses navigate their insurance needs confidently.

Why should I choose EG Bowman as my insurance agency?

At EG Bowman, we combine decades of expertise with a client-focused approach to provide unparalleled service. Unlike larger, faceless companies, we build long-term relationships with our clients, offering personalized advice and solutions. We prioritize your needs, shop for the best rates, and advocate on your behalf when it comes to claims. Our goal is to be your trusted advisor in navigating insurance complexities and ensuring peace of mind.

How can I get a quote for insurance through EG Bowman?

Getting a quote with EG Bowman is simple and hassle-free. You can call us directly at 212-425-8150 or email us at info@egbowman.com to discuss your insurance needs. Our team will gather information about your situation and compare policies from multiple carriers to provide the best options. Whether it’s personal or business insurance, we ensure the process is transparent, efficient, and tailored to you.

Does EG Bowman offer insurance for small businesses?

Yes, EG Bowman specializes in working with small businesses. We understand the unique challenges small businesses face, from managing risks to staying within budget. Our insurance solutions cover everything from general liability to property insurance and more. By tailoring policies to fit your specific needs, we ensure your small business is well-protected while keeping costs manageable.

FAQS PAGE

Frequently Asked Questions

We understand you may have questions about our insurance services and how we can help protect what matters most to you. Below, you'll find answers to some of the most common questions we receive. If you don’t see the information you’re looking for, feel free to reach out to us directly. Our team is here to assist you with personalized advice and solutions.

NEWS & BLOG

Explore Our New York Insurance Blog

Contact Us